South to Put Off Rising Again

Despite some other increase to the Official Cash Rate, paying off a mortgage is still preferable than staying in the apace rising rental market

Another OCR rise won't dent the enthusiasm in the property market place, says Century 21 New Zealand Possessor Tim Kearins.

"That's because for the likes of first-home buyers paying a mortgage remains comparable, or even cheaper, than paying the tape-high rents we're seeing nationwide."

On November 24 the Reserve Bank once once again lifted the Official Greenbacks Rate past another 25 basis-points to 0.75% – marking the second consecutive OCR hike by the central bank in over seven years.

"While banks have already increased their involvement rates in apprehension, they're still heading on an upwards track. That will only see buyers more motivated to act, making the near of low involvement rates this summer.

"People are waking upwards to the fact that they can either purchase and set their interest charge per unit at say four.5% or wait and pay 6% – which is 33.3% more. Further, many pundits doubt property prices volition drop, so waiting is now not much of an option.

Meanwhile, Trade Me last calendar week released its latest Rental Price Index which confirmed national rents striking new highs, with the median weekly rent on its site at $560 in October – up viii% in 12 months. At the same time Auckland's median advertised weekly rent hit $600.

"Those contemplating selling their properties tin can at present likewise encounter it will be a strong summertime, while 2022 remains not and so articulate," says Kearins.

"Hence Century 21 is expecting many Kiwis to push play on selling their property in the adjacent 2 or three months."

CoreLogic NZ Chief Belongings Economist Kelvin Davidson says attention will now quickly turn to what'due south next, and when/how loftier the peak for the OCR might ultimately exist.

"The forecasts from the RBNZ suggest a tiptop of around 2.5% in late 2023, but yous'd accept to think that this peak could be reached sooner and/or exist higher, peculiarly with the declaration from Regime that borders will reopen in the first half of 2022.

"For the residential property marketplace, the implications are articulate – in that location are further mortgage interest charge per unit increases to come. With most shorter term fixed rates now pushing up towards (or above) the 4% mark, nosotros've already seen them pretty much double from the previous lows, and figures of 5% or more than wouldn't be a surprise over the next half dozen-12 months either.

"Of course, that'due south still low by past standards. And borrowers rolling off loans agreed peradventure two years ago, and/or who kept their repayments the same even as rates roughshod in 2020, may not see much change.

"Nevertheless, many borrowers on rolling one-year terms could meet a significant shift in mortgage costs. In fact, according to RBNZ information, $227.8bn in mortgages are either floating or due to roll over in the next twelvemonth. This equates to 71% of all lending – a lot of funding which when refixed will probable lead to greater mortgage repayments and afterwards less disposable income.

"Overall, with unemployment still low, the housing marketplace isn't necessarily headed for a crunch. But there are certainly headwinds (e.1000. higher mortgage rates, and tighter lending rules such as potential debt to income ratio caps) which will likely lead to a slowdown in sales volumes and a reduction in the pace of value growth throughout 2022."

Kearins says Reserve Depository financial institution hikes will not deter commencement-home buyers from purchasing holding and locking in some good, fixed rates, as evidenced by CoreLogic's latest bi-almanacStarting time Home Buyer Report.

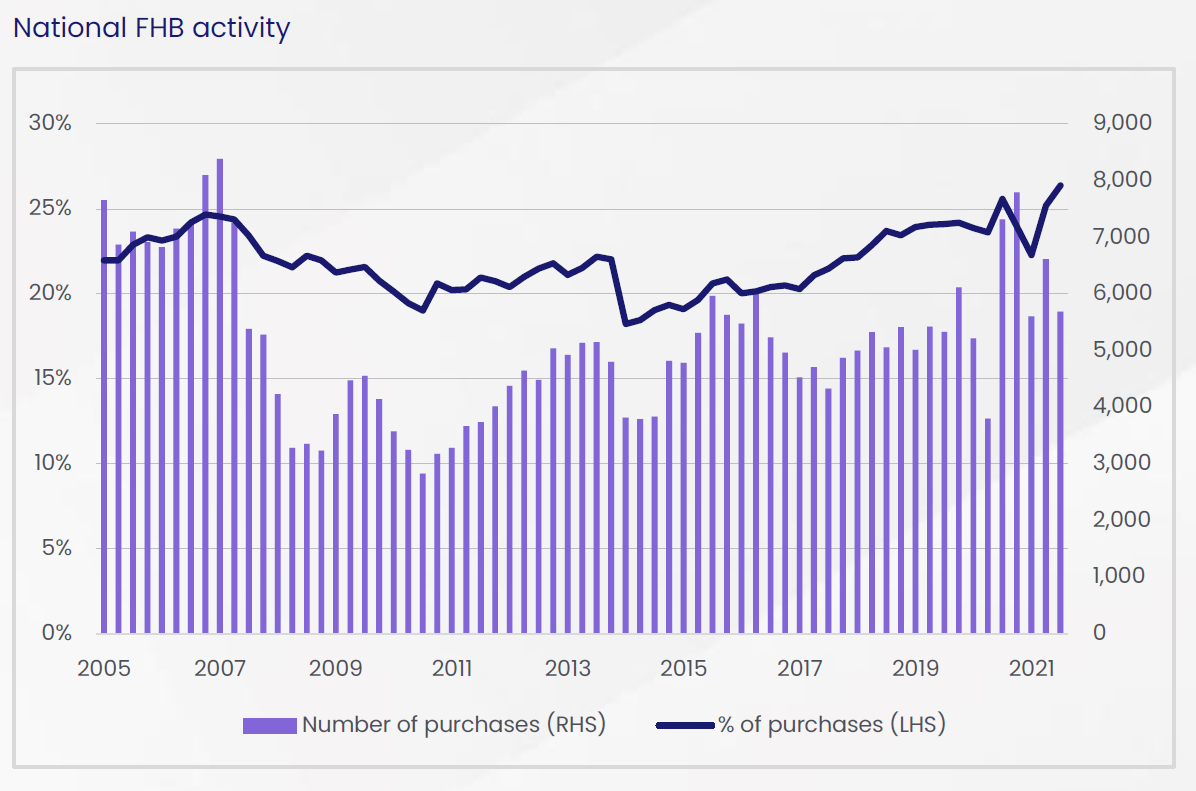

New Zealand first dwelling buyers (FHBs) take hit tape high market share over the third quarter of 2021, despite tough market conditions and rapidly rising house prices.

26.4% of all buyers in the iii months to 30 September, 2021 bought a property for the kickoff fourth dimension, completing about 5,700 transactions.

During the same three-month catamenia CoreLogic's Business firm Price Alphabetize revealed New Zealand'south average property value increased four.8% to $950,229, upward 27.8% for the 12 months to the finish of September. Values rose a farther ii.1% in October.

Davidson says the proportion of FHBs in the market betwixt July and September 2021 was well above the long-term average of 21.viii% and surpassed the previous benchmark of 25.6% ready in the third quarter of 2020.

"We have to admit that the underlying number of transactions has been disrupted by COVID and the lockdowns over August/September, so we need to take a petty extra care when interpreting marketplace share figures," he says.

"However, information technology'southward rubber to say FHBs are very agile in the marketplace. The number of deals they were involved with in Q3 was the highest for the tertiary quarter of whatsoever year since 2015, except for the same catamenia last year, when nosotros saw the figures 'artificially' pushed upwards due to the postal service-lockdown bounce."

Despite the widespread boom in house price growth and associated larger deposits, Davidson says the share of purchases being fabricated by FHBs has been unexpectedly strong in the past few months.

"One of the biggest barriers to abode ownership is saving a deposit and in the past yr it'south go progressively harder for aspiring FHBs to become those funds together," Davidson says.

"The boilerplate fourth dimension to save a eolith is at present more than 10.5 years, up from less than 9 a year agone, and well to a higher place the long-term average of around eight years. Ownership with a eolith that's less than the standard 20% has previously been popular among FHBs. Notwithstanding since the banks' allowance for advancing low deposit loans to possessor occupiers recently halved from xx% of lending flows to x% that is no longer an selection for many."

KiwiSaver, which is being utilised for a home eolith, has been a key source of support for buyers Davidson says, while the trend among FHBs to compromise either on the type of belongings and/or location is gaining momentum.

Based on the CoreLogic Heir-apparent Nomenclature serial, the Q3 2021 Outset Abode Heir-apparent Report analyses FHB activeness in each function of the land. The report includes details on locations, prices paid and what types of properties FHBs purchased in the iii months to September 30, 2021.

FHBs are divers as having never previously endemic property in New Zealand before and a mortgage has been secured against the property to complete the transaction.

The national trends have been replicated beyond Auckland,Hamilton, Tauranga, wider Wellington, Christchurch, and Dunedin, as FHBs' market share in the quarter registered above long-term averages by at least two pct points.

Wellingtonrecorded the highest share of FHB action at 33% in Q3 2021, compared to the city's long-term boilerplate of 29%.Dunedinrecorded the virtually significant growth, registering a FHB market share figure of thirty%, eight pct points above its average of 22%.

Beginning time belongings owners are paying slightly less than the residue of the market, notably in the country's nearly expensive cityAuckland, where FHBs paid a median price of $900,500 in Q3 2021. The figure is $149,500 less than the median price being paid by all buyers ($i,050,000) in Auckland.

The gap was also more than than $100,000 inTauranga, where FHBs paid a median price of $760,000 compared to Wellington, where $800,000 was the median toll paid to become into the market.

FHBs inChristchurchpaid a median price in excess of $500,000, simply the figure remains lower than Dunedin, where the median price paid during the quarter was $566,125.

The nigh expensive FHB market across NZ's primary urban areas wasQueenstown, where a median price of $860,000 was paid by FHBs, followed byKapiti Coast at $777,500 andPalmerston Northward,Whangarei,Napier, andNelsonwhere FHBs paid more than $600,000. Amid the chief urban areas,Invercargillwas the country'due south lowest priced FHB market, with a median of $382,000 in Q3 2021.

Freestanding houses accounted for 72% of FHB purchases in Q3 2021, downwardly sharply from the total-year effigy of 78% in 2020, every bit affordability constraints forced buyers to consider flats. The percentage of flats – divers as townhouses and other shared wall properties – purchased past FHBs was 18%, upwards from fourteen% last year.

Davidson says FHBs were taking the opportunity to get into the marketplace, capitalising on strong fiscal incentives to purchase rather than rent, filling the gap left past a pass up in mortgaged investors' marketplace share who faced tougher atmospheric condition due to tighter lending restrictions.

"Information technology will exist interesting to encounter if the FHB market share tin hold up at similar levels in the coming quarters, given that the depression eolith lending speed limit is at present much tighter," he says.

Key insights from this report include:

- From July to September 2021, FHBs had a market place share of purchases of 26.4% – well to a higher place the average of 21.8%, and moreover a new record loftier.

- On boilerplate a FHB requires 10.5 years to relieve a deposit.

- Auckland FHBs spent a median $900,500 in Q3 2021 to get into the market compared to those in Invercargill, who spent $382,000.

- Standalone houses accounted for 72% of FHB purchases in Q3 2021 – downwards sharply from the full-yr figure of 78% in 2020.

- FHBs accept purchased relatively more than flats (normally a property with a shared wall that isn't an apartment), with this belongings type now accounting for 18% of their activity, upwards from 14% terminal year.

- The median price paid by FHBs in Q3 2021 was $660,000, up from the figure of $565,000 for 2020 as a whole, but lower than Q2 2021'south number of $685,000 – when houses were a larger share of their purchases.

Source: https://www.propertyandbuild.com/first-home-buyers-not-put-off-rising-mortgage-rates/

0 Response to "South to Put Off Rising Again"

Postar um comentário